by Pieter Fourie, CFA, Head of Global Equities

The Sanlam Global High Quality fund invests in high quality businesses with a long term time horizon, and adds value through active management. It invests with no reference to the index, focusing on businesses with durable business models. Since inception, the investment philosophy of the Fund has remained unchanged.

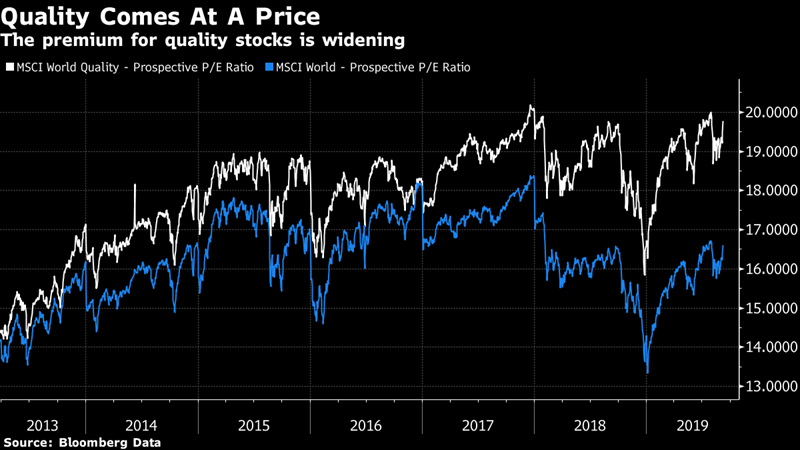

A major challenge facing quality investors at the moment is that they are paying a record premium for the safety of strong balance sheets and reliable profitability. The following chart shows Bloomberg’s prospective P/E multiple for the MSCI World Quality index and the main World index over the last 7 years. The Quality index sells for 19 times next year’s earnings, compared to 16 times for the index as a whole – a big and widening premium:

We remain in an environment where slowing economic growth and pressure on margins make it tougher for companies to deliver on earnings expectations. However, it is pleasing to see that those businesses that can deliver are being rewarded via increasing share prices, and we continue to put great emphasis on selecting stocks that can execute their business plans regardless of the economic uncertainty.

We follow an approach which allows us to wait patiently to enter positions in companies which we cover from our universe of roughly 120 names.

Recent examples of stocks which have performed well for us include Medtronic, Bayer, Allergan and Intercontinental Hotels.

Medtronic posted strong results, with organic growth of 3.5% and all four of the company's main operating segments beating the market’s expectations. The company’s good start to its fiscal year was reaffirmed by management maintaining their yearly guidance of 4.0% organic growth. The anticipation of the forthcoming unveiling of the company’s long awaited surgical robot platform and several pipeline assets launching have helped to support near term expectations. Looking at the valuation range of Medtronic we do notice that the company is now trading towards the upper end of the range and we have started to reduce the position.

Bayer rallied +13.6% in August as the beneficiary of a couple of pieces of company-specific good news. The first bit of news was a rumour that Bayer had reportedly agreed to pay $8 billion to settle thousands of lawsuits alleging that Roundup weed killers (that they inherited in their Monsanto acquisition) caused cancer. This was seen as positive news by the market primarily due to the removal of that particular overhang, even though the settlement was higher than sell-side analysts had assumed. The second bit of positive news for Bayer was the sale of their animal health business for €6.9 billion, higher than market expectations. This will go some way to paying down the company debt as well as simplifying the business.

Allergan was a new addition to the portfolio last year and in the last week of June, the US pharmaceutical company finished up close to 40%, moving our holding to a top 10 position in the fund. At the time of our initial investment we highlighted that Allergan’s competitive advantage lies in the brands it owns, including Botox as well as some other durable premier brands in the aesthetics space. We believed the durability of these franchises was being overlooked by the market after a few disappointing years of performance.

The fact that a competitor (AbbVie) recognised the value in Allergan at $130 per share and decided to purchase the company is pleasing to the extent that we kept increasing our position whilst the stock was weak earlier in the year.

Intercontinental Hotels Group (IHG) has a very strong brand across its portfolio with the Holiday Inn Brand the largest hotel brand in the world. The company is well positioned in all major markets with their predominant focus on the Americas region. We expect IHG’s growth opportunities in Asia to meaningfully contribute to the group’s earnings potential over the next decade and beyond. IHG has an attractive recurring-fee business model with low capital requirements. The asset-light business model generates about 95% of its cash flow from franchised and managed hotels with these two segments making up 99% of rooms in the group.

Intercontinental generates close to a 50% return on capital and the free cash flow yield of 5.5% is in line with the average free cash flow yield of the fund. If our forecasts are accurate the average free cash flow yield for the group over the next 5 years would be close to 7.0% from today’s share price levels.

By bringing in new names in to the portfolio we continue to maintain our valuation discipline on the fund even in the face of ever increasing multiples for high quality businesses.

Important Information

The Fund may invest in companies based in emerging markets which may involve additional risks not typically associated with other more established markets such as increased risk of social, economic and political uncertainty. The Fund has holdings which are denominated in currencies other than sterling and may be affected by movements in exchange rates. Consequently the value of an investment may rise or fall in line with the exchange rates.

The value of this portfolio is subject to fluctuation and past performance is not necessarily a guide to future performance. The performance is calculated for the portfolio and the actual individual investor performance will differ as a result of initial fees, the actual investment date, the date of reinvestment and dividend withholding tax. All terms exclude costs. Fluctuations or movements in exchange rates may cause the value of underlying investments to go up or down. Do remember that the value of participatory interests or the investment and the income generated from them may go down as well as up and is not guaranteed, therefore, you may not get back the amount originally invested and potentially risk total loss of capital. Therefore, the Manager does not provide any guarantee either with respect to the capital or the return of a portfolio. The Manager has the right to close any Portfolios to new investors to manage them more efficiently in accordance with their mandates. Collective Investment Schemes are traded at ruling prices and can engage in borrowing and scrip lending. Collective Investment Schemes (CIS) are generally medium to long term investments. A schedule of fees and charges and maximum commissions is available on request free of charge from the Manager, the Investment Manager or at www.sanlam.ie.

Issued and approved by Sanlam Investments. Sanlam Investments is the trading name for our two Financial Conduct Authority (FCA) regulated entities: Sanlam Investments UK Limited (FRN 459237), having its registered office at 24 Monument Street, London, EC3R 8AJ and Sanlam Private Investments (UK) Ltd (FRN 122588) having its registered office at 16 South Park, Sevenoaks, Kent, TN13 1AN.

The Fund is a sub-fund of the Sanlam Universal Funds plc, a company incorporated with limited liability as an open-ended umbrella investment company with variable capital and segregated liability between sub-funds under the laws of Ireland and authorised by the Central Bank. The Fund is managed by Sanlam Asset Management (Ireland) Limited, Beech House, Beech Hill Road, Dublin 4, Ireland, Tel + 353 1 205 3510, Fax + 353 1 205 3521 which is authorised by the Central Bank of Ireland, as a UCITS Management Company and Alternative Investment Fund Manager, and is licensed as a Financial Service Provider in terms of Section 8 of the South African FAIS Act of 2002. Sanlam Asset Management is a registered business name of Sanlam Asset Management (Ireland) Limited. Sanlam Asset Management (Ireland) has appointed Sanlam Investments UK Ltd or Sanlam Private Investments (UK) Ltd as Investment Manager to this fund.

This document is provided to give an indication of the investment and does not constitute an offer/invitation to sell or buy any securities in any fund managed by us nor a solicitation to purchase securities in any company or investment product. It does not form part of any contract for the sale or purchase of any investment. The information contained in this document is for guidance only and does not constitute financial advice.

The fund price is calculated on a net asset value basis, which is the total value of all assets in the portfolio including any income and expense accruals. Trail commission and incentives may be paid and are for the account of the manager. Performance figures quoted are from Sanlam and are shown net of fees. Performance figures for periods longer than 12 months are annualized. NAV to NAV figures are used. Calculations are based on a lump sum investment.

Please note that all Sanlam Funds carry some degree of risks which may have an adverse effect on the future value of your investment. Any offering is made only pursuant to the relevant offering document, together with the current financial statements of the relevant fund, and the relevant subscription/application forms, all of which must be read in their entirety together with the Sanlam Universal Funds plc prospectus, the Fund supplement and the KIID. All these documents explain different types of specific risks associated with the investment portfolio of each of our products and are available free of charge from the Manager or at www.sanlam.ie. No offer to purchase securities will be made or accepted prior to receipt by the offeree of these documents, and the completion of all appropriate documentation. Use or rely on this information at your own risk. Independent professional financial advice should always be sought before making an investment decision as not all investments are suitable for all investors. _SAH0919(101)1219UKInst